Market Observations

Fed Cutting Rates - Investing in Overvalued Market?

Welcome back,

If this is your first time reading these posts, thank you for reading. I have a passion for the markets and people. In writing this weekly post I am able to keep myself accountable by diving deeper into topics than just headlines, and hopefully provide you some value in your own research or interests.

I believe money is a tool, given from God, to accomplish his purposes. The Bible has 2,350 verses about money. How should we handle our money knowing it is a topic of upmost importance to God? Did you know that investing is Biblical? The Bible calls us to be both stewards and multipliers of money (Matthew 25), as well as generously open handed with our money (Proverbs 11), but ultimately the Bible calls us to be on guard against this tool attempting to fill a hole in our heart that only Jesus can fill (James 3 - Exodus 20 - Matthew 6).

Regarding my passion for people, I believe we live in a time period that will be looked back on as an information and entertainment glut. While entertainment in itself is not bad, entertainment in subjects like economics, politics, and public information (news/MSM) is slowly eroding a generations ability to think critically for themselves, me included. Gen Z is now nicknamed “the anxious” generation, this should be no surprise as 7+ hours a day are spent in gazing/scrolling into comparison and self absorption. In fact if you’ve made it this far, congrats, with an average attention span of eight seconds I shouldn’t expect you to get past the first paragraph!

Today, you will see 5,000+ advertisements, targeting your deepest vulnerabilities to drive you to make decisions, or condition you to make a decision into the future. This weekly article has no strings attached. I am genuinely interested in the pursuit of critical thinking and learning for both myself and you, so we can be better stewards of money.

Reach out to me anytime.

Fed Interest Rates Explained

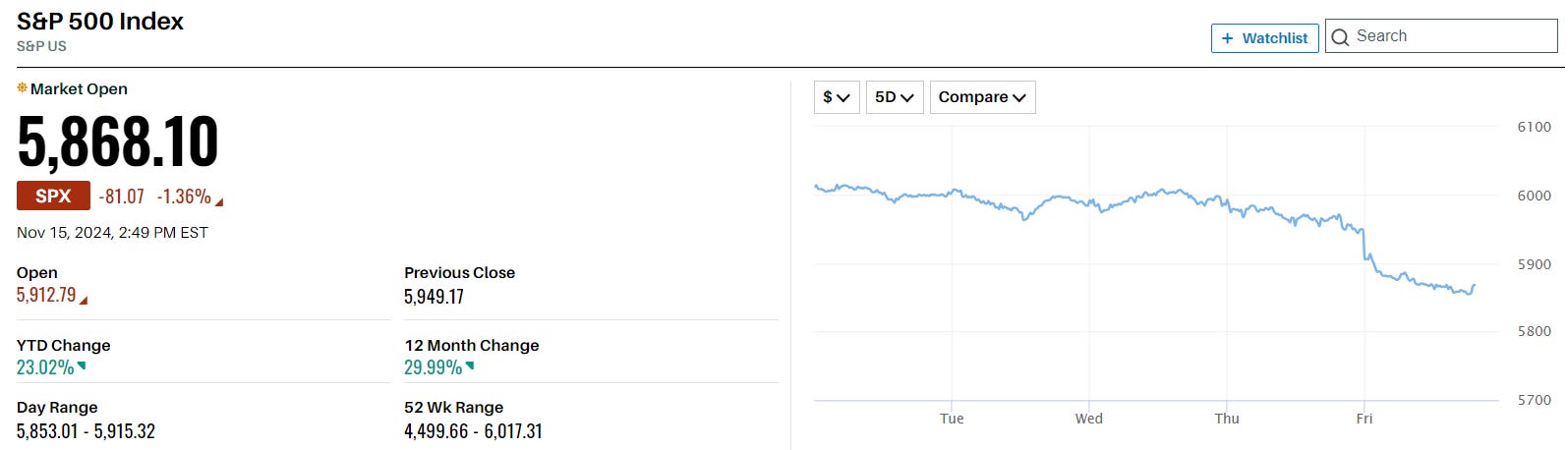

The Fed continues to fight inflation down to 2% from highs of 7.2% in 2022. The Fed recently cut interest rates down from 5.33% to a target range of 4.5%-4.75%. Although they are expected to keep dropping rates, Powell has mentioned he is not in a hurry to cut, due to threats of inflation rising. As you can see the market wants rate cuts, and did not respond well on Friday to Powell taking his time.

The above graph of the Fed funds interest rate is an extremely important indicator to understand, and it is also very simple to understand. Businesses use debt to grow, they will take out loans to buy equipment, inventory, acquiring other businesses, etc. The rate of interest at which they pay back the loan is dependent on what the bank can lend their money to other banks “risk-free”. The higher the interest rate, the more difficult it is for businesses to get loans and grow, meaning the value of the business fall from slowing growth. The opposite is also true, when interest rates fall, businesses are more able to afford taking on a loan to grow and the value of the business increases on growth assumptions.

The Fed raised interest rates in 2022 to slow inflation, which was at 7.2%, and is now cutting rates to re-accelerate growth now that inflation is near 2%. The market is currently pricing in another 25 basis point (.25%) cut in December, but Powell has mentioned his sole emphasis is employment.

Investing in An Overvalued Market

I am including a chart below of sector performance by ETF’s over the last three months.

Top Three Gainers:

XLY - Consumer Discretionary

XLF - Financials/Banks

XLC - Communications

Top Three Losers:

XLV - Healthcare

XLP - Consumer Staples

XLRE - Real Estate

Although some sectors are doing better than others this year, the total market has offered a wonderful return. When the market runs like it has this year, it is easy to think one of two things. (1) The market is ripping, rates are dropping, Trump is in office, its a great time to invest, or (2) The market is overvalued, I am going to wait for the next pull-back or crash to get in.

Both responses are understandable reactions, but both are naive. On one hand, the market is undervalued….IN COMPARISON…to historical market valuations. The market does not care that you think it is expensive, and it will remain irrational longer than you can bear it. A quick way to see valuation is by taking the value of the total US market, and dividing it by GDP.

Based on the above chart, it feels like you should wait to invest until it gets back to normal levels…. well… “normal” levels haven’t been touched since 2015. Based on this chart alone, you will have missed hundreds of %’s of growth. On the flip side, if you invested in the top of the market in 2000 (tech bubble) you will have no made your money back for 13 years, as well as enduring the 2008 bubble. There is something to be said about waiting, just as much as investing.

So what do we do? My approach has been to dollar cost average. Whether the market goes up, or goes down, you are putting in money and averaging out your cost basis. Over all you are not betting on the business & credit cycle, but the US economy in the long run. This argument is a little different for single stocks, if interested reach out to me and would love to talk ideas.

Here is also a great article on dividend growers, who no matter what the market is doing, aim to pay you for holding their stock. I also wrote about this kind of investing previously. Time in the market beats TIMING the market.

Thank you for tuning in this week, remember, the market is a tool to use, not a teacher to direct you. Just like in baseball, Mr. Market throws you thousands of pitches everyday and you get to decide which ones you hit, luckily in investing you can’t strike out.