Investment Process Overview

New Thoughts

No company deep-dive this week, but I have spent time recently, and will forever spend time, critiquing my decision making process and the specific measures I am looking at when looking at a business.

I wanted to shares a few points on process and how I am tweaking the specific measures I am looking at, to try and find great businesses to buy at fair prices, and sometimes buy fair businesses at great prices.

Five Important Measures:

The industry

The narrative

The numbers

The value

The management

The Industry

The industry is one of the first steps in the investment process. I start off looking at every single industry and try to understand which ones are growing, which ones are declining, and which ones are maturing. Much of the industry performance is apart of the overall cycle, a lot of times having to do with availability of credit.

Not to get too off track but the degree of availability of credit (or debt) allows businesses to expand or forces them to constrict. Businesses will use debt to expand capital investments on which they bet to make a higher return (ROIC) than the interest they pay out on the debt. For example a project that will return 10% on the new machinery in operating profit, while paying 4% on the term loan to buy it, is a good project for management.

Some of the hottest sectors attracting most of the capital investment over the last two decades have been tech (by a lot), discretionary businesses, and healthcare.

Some of the weakest sectors in the last two decades have been REITS, Communications, and energy.

It is important to understand secular trends in the market to find some investable businesses. 50 years from now, which sectors will be receiving government investment, providing value to consumers, and contributing to infrastructure?

The Narrative

The narrative of a business is the story behind the numbers. Aswath Damodaran gives a great talk in the hyperlink about the value of stories in businesses. Damodaran gives an example of venture capital firms, who invest mainly on stories, while banks or mature financial institutions invest solely on numbers.

Naturally I am a numbers person, and am skeptical of businesses that are over leveraged and hoping for profits one day. I will receive less return for less risk, but I have found that is where I am comfortable.

When looking at a business I want to understand how they were started, some of their main challenges, and where they are planning to go. For example some simple stories to understand is CAVA 0.00%↑ who has announced they want to go from 309 restaurants to 1000 by 2032, and promote heart healthy Mediterranean food along the way. This mission matches the Millennial and Gen Z crowd who is the generation most likely to ‘say’ that’s important to them.

The Numbers

After finding an interesting business with a story that is continuing to unfold, I like to understand its financial history. I like to know what their revenue growth has been like, what are their margins, which expenses are contributing most to those margins, do they have positive free cash flow, and if so, how are they re-investing that, do they pay a dividend, if not what initiatives are they investing it to contribute to shareholder value?

Lots of questions but each step takes just a few minutes. The annual report of a company has a section called management discussion of financial results, and in that they explain almost all the line items and how each contributes to their financial success.

The Value

Now this…. is where I spend most of my time.

Finding value answers the question, how much should I pay for a share (partial ownership) of this business?

If you see a neighborhood offering a lemonade stand up for sale, how much do you pay for it? One way is to just match the lemons, chairs, and table to what you could buy at Walmart and pay for that. Another, more accurate way for the seller, is to project all the cash the stand would make as profit, not revenue, from now until Jesus comes back, and discount it back at a rate to reflect risk and opportunity cost.

Practically you can find how to do that HERE.

I have also come across an interest expected rate of return formula with QuantCompounder from Base Hit Investing .

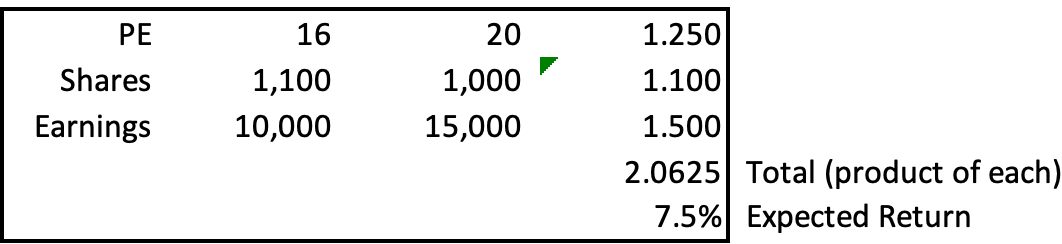

The three engines of growth formula was created by John Huber from Saber Capital Management and is a very practical take on the shareholder return formula. You make some future assumptions by taking the PE you expect the company to trade at in 10 years, the total shares outstanding in 10 years, and the net income in 10 years and divide each one by the present day number.

Shown practically below, reach out with any questions. This is an example case and would not be enough return for me to want to invest, I would want something over 12% with conservative assumptions.

See a better explanation from John HERE.

Management Teams

Management is a very important aspect of the investment decision making process and could just as easily be put at number one on the list of importance. If management is incompetent or immoral in character, the valuation, industry, and story of the company don’t matter.

Judging these management teams is very difficult as I don’t have a very extensive history on seeing great managers vs poor managers. I am continuing to learn about things to look for and do not feel as comfortable to guide others on how to do this, so I will attach a helpful source HERE.

Ultimately after character, I want to see how they view shareholders, and if shareholder value is important to them. Are they paying out higher salaries and bonuses or are they paying out dividends and buying back stock?

Thank you all again for reading.

Feel free to find me on Twitter HERE

Subscribe for a free stock value tool below.

Thanks for the shoutout! Great post